Opening marker: QSR credit ratings can help a NNN buyer separate brand strength from lease risk, but they do not replace property-level underwriting.

Quick-service restaurant real estate is one of the most familiar corners of the net lease market. The buildings are simple. The brands are visible. The leases often run long. The income story is easy to explain to a 1031 buyer who wants passive rent without learning a new operating business.

That familiarity is useful. It is also dangerous.

A McDonald’s ground lease, a Starbucks corporate lease, a Taco Bell franchisee lease, a Wendy’s box in a slowing trade area, and a Burger King leased to a thinly capitalized operator may all sit inside the QSR category. They do not carry the same credit risk. They do not deserve the same cap rate. They do not create the same exit audience.

Credit ratings are one of the best starting points for separating those risks because they force the buyer to ask a basic question: whose balance sheet am I actually depending on? But in restaurant NNN real estate, the answer is rarely as simple as the logo on the building.

For private buyers, the underwriting job is to connect four layers: public credit, lease obligor, unit economics, and residual real estate. Miss one layer and the cap rate can lie to you.

Credit ratings measure enterprise risk, not automatically lease risk

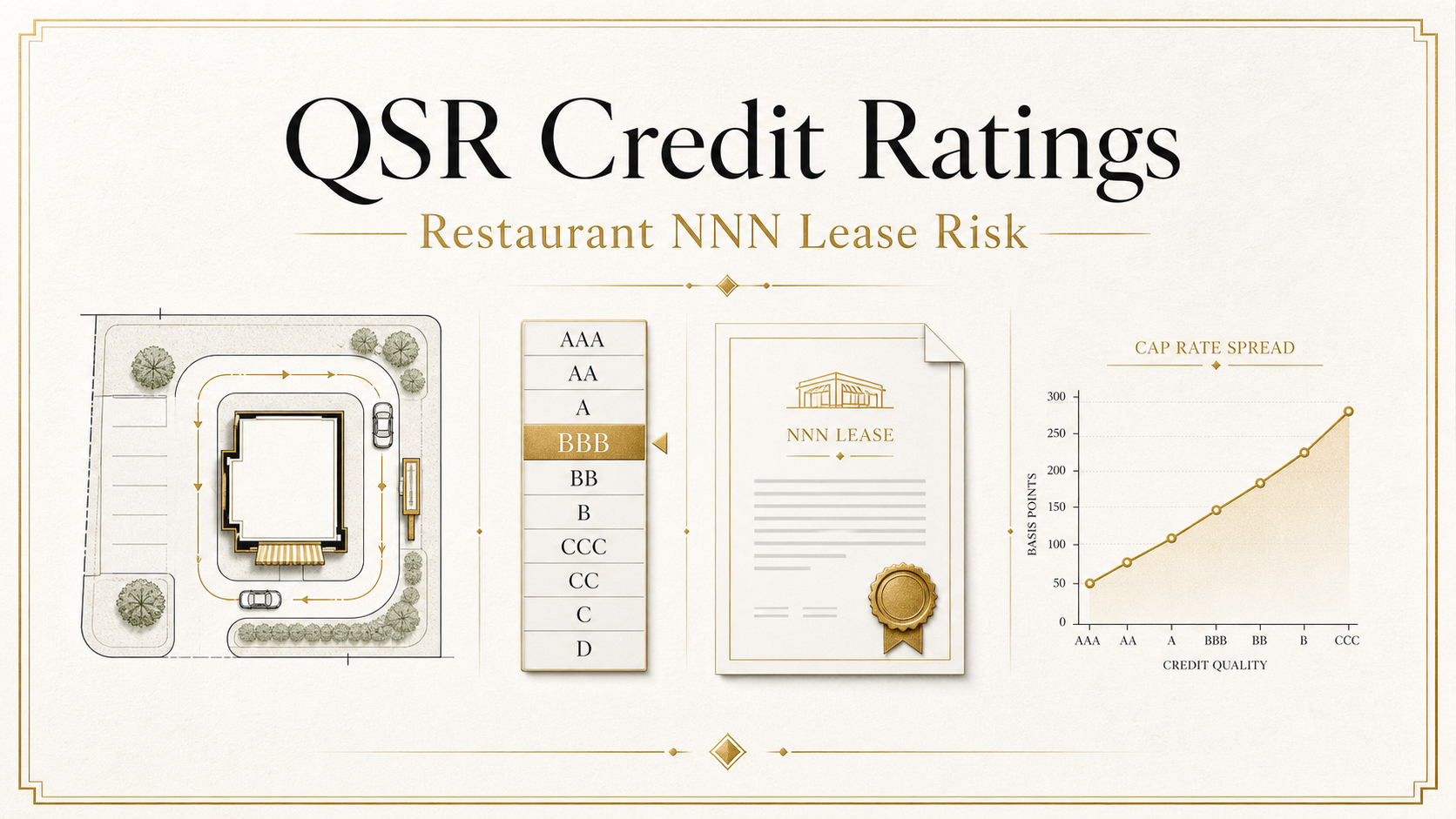

S&P, Moody’s, and Fitch credit ratings are opinions about an issuer’s ability and willingness to meet financial obligations. They are useful because they compress a large amount of public-company credit analysis into a common language. Investment grade generally begins at BBB- or Baa3. Below that line, the issuer is non-investment grade or speculative grade.

That framework matters in QSR because the restaurant sector includes some of the most recognizable public companies in the world. McDonald’s, Starbucks, Yum! Brands, Restaurant Brands International, and other large systems have public filings, debt disclosures, rating histories, and analyst coverage. A buyer can look at leverage, cash flow, franchise mix, comparable sales, store growth, and capital allocation with much more transparency than is available for a private franchisee.

But a corporate credit rating does not automatically attach itself to every restaurant with that brand name on the wall.

The rated issuer may be the parent company. The tenant under the lease may be a subsidiary, a franchisee operating company, a single-purpose LLC, or a local franchise group. The guarantor may be the public company, an affiliate, a holding company, an individual owner, or nobody beyond the tenant entity. Those distinctions are not legal trivia. They are the credit stack.

A rated brand can support demand, franchisee depth, lender confidence, and resale liquidity. It does not automatically guarantee the rent unless the lease documents say so.

That is the first rule of QSR NNN credit analysis: start with the signer, not the sign.

Why the QSR spread is so wide inside one category

The net lease market already prices this difference. The Boulder Group’s Q1 2026 net lease research showed corporate QSR assets around a 5.82% national asking cap rate and franchisee QSR assets closer to 6.80%. That is nearly 100 basis points of spread inside the same restaurant category.

The tenant-level examples make the pattern clearer. Boulder’s Q1 2026 tenant profile work showed McDonald’s ground leases around 4.40%, Chick-fil-A ground leases around 4.50%, Chipotle around 5.45%, Taco Bell around 5.50%, Wendy’s around 5.73%, Dunkin’ around 6.10%, Burger King around 6.40%, Starbucks around 6.45%, and KFC around 6.50%.

Those figures are not a promise about any individual property. A specific asset can price tighter or wider based on market, rent, lease term, rent bumps, store sales, construction, parcel quality, financing, and buyer demand. But the spread itself is telling.

The market is not merely buying hamburgers, coffee, chicken, or tacos. It is pricing a bundle of risks:

- the enterprise credit behind the concept

- the lease party and guarantor

- the operator’s ability to pay rent

- the site’s sales productivity

- the durability of the drive-thru or restaurant format

- the replacement tenant pool if the current use fails

- the buyer universe at resale

That is why a 6.40% Burger King lease is not automatically better than a 4.40% McDonald’s ground lease. The extra yield may be compensation for weaker credit support, shorter lease term, private franchisee opacity, higher unit risk, or less liquid exit demand. It may also be a fair risk-adjusted return if the operator, rent coverage, and site quality are strong.

The cap rate is an output. Credit analysis helps explain the input.

McDonald’s: the benchmark, but still document-dependent

McDonald’s is the cleanest example of how public credit and real estate structure can create premium NNN pricing. InvestmentGrade.com’s tenant profile lists McDonald’s at BBB+ from S&P and Baa1 from Moody’s, both investment grade, with a stable outlook in the latest profile data. The company’s public filings describe a heavily franchised system, with roughly 95% of restaurants franchised at year-end 2024. That model produces royalties and rent streams that are not identical to the economics of a single restaurant tenant.

For NNN buyers, McDonald’s also has an unusually deep real estate story. Many McDonald’s assets are structured as ground leases, and the company has long used control of restaurant real estate as part of its operating system. A strong McDonald’s ground lease can therefore combine a recognizable public credit, a long lease, a simple building or ground lease format, high franchisee demand, and a broad buyer pool.

That is why the best McDonald’s NNN assets can price like bond-adjacent real estate.

But even here, lazy underwriting is expensive. A buyer still has to confirm whether the lease is directly with McDonald’s Corporation, a corporate affiliate, or a franchisee entity. A ground lease is different from a fee-simple building lease. A 20-year lease is different from an eight-year lease. A hard corner with durable drive-thru demand is different from a tertiary site dependent on one traffic generator.

The McDonald’s name can make the diligence more attractive. It does not make diligence optional.

Starbucks: investment grade credit with shorter-format lease questions

Starbucks is also investment grade in InvestmentGrade.com’s tenant profile, listed at BBB+ and Baa1. The public credit story is strong relative to most restaurant tenants: global brand power, large revenue base, institutional reporting, and a corporate guarantee in many marketed NNN structures.

For a private buyer, however, Starbucks underwriting often looks different from McDonald’s underwriting. Starbucks leases frequently have shorter initial terms than the classic 20-year QSR ground lease. The boxes can be inline, end-cap, drive-thru, freestanding, or part of a broader retail project. Store performance can vary meaningfully by commute pattern, drive-thru availability, labor market, and local consumer behavior.

That means the credit rating helps answer one question but not all questions.

If the lease is genuinely backed by Starbucks Corporation, the corporate credit can support financing and resale demand. But the buyer still has to underwrite remaining term, rent level, renewal probability, access, format, and replacement demand. A ten-year Starbucks with excellent drive-thru geometry and conservative rent is a different asset than a short-term cafe in a weaker retail corridor.

The public rating improves the credit lens. The real estate still decides the downside.

Yum, RBI, and the franchisee problem

Yum! Brands and Restaurant Brands International are central to QSR NNN investing because their systems include many of the brands investors see in net lease listings: Taco Bell, KFC, Pizza Hut, Burger King, Popeyes, Tim Hortons, Firehouse Subs, and others. These public companies may have rated debt and substantial enterprise value. But many restaurant leases in those systems are not direct parent-company leases.

That is the core franchisee problem.

A Taco Bell, KFC, Burger King, Popeyes, or Dunkin’ property may be operated by a large, experienced, multi-unit franchisee. It may also be leased to a small operator with limited financial disclosure. The franchisor controls the brand and receives royalties. The landlord receives rent from the tenant named in the lease.

Those two facts can point to different credits.

This is why QSR franchisee leases often need a larger spread than corporate leases. The buyer is not only accepting restaurant operating risk. The buyer is accepting less public information, more dependence on unit-level economics, and a narrower resale audience if the guaranty stack is thin.

A franchisee lease can still be a strong NNN investment when the operator is well capitalized, the guarantor is meaningful, store sales are strong, rent is sustainable, and the site has durable drive-thru value. The problem is not franchisee credit. The problem is paying corporate-credit pricing for franchisee-credit documents.

Restaurant lease risk is really four risks stacked together

A disciplined QSR buyer should separate restaurant NNN risk into four buckets.

1. Enterprise credit risk

This is the public-company or system-level story. Is the brand growing or shrinking? Is leverage manageable? Are comparable sales stable? Are margins under pressure? Does the company have access to capital? Are rating agencies stable, negative, or improving on the credit?

For rated QSR companies, this layer is relatively transparent. For private franchisees, it is much harder.

2. Lease obligor and guarantor risk

This is the document-level credit story. Who is the tenant? Who guarantees the lease? Does the guaranty cover payment only or broader performance obligations? Does it last for the full term? Does it survive assignment? Is it limited by dollar amount, time, or entity structure?

This layer is where many buyers accidentally import the brand’s credit into a lease that the brand did not sign.

3. Unit economics risk

Restaurants pay rent from store-level cash flow. Labor, food costs, delivery-app economics, remodel obligations, royalties, local competition, and traffic patterns all matter. A strong corporate credit can absorb weak units. A thin franchisee may not.

If store sales are available, rent coverage should be a primary underwriting line. If sales are not available, the buyer should lean harder on rent comparables, operator financials, site quality, and conservative downside assumptions.

4. Residual real estate risk

If the tenant leaves, what is left? A great drive-thru parcel with access, visibility, parking, and flexible zoning may have multiple replacement users. A specialized box on an awkward parcel may have a narrower path. The lease income may be bond-like while it lasts, but the real estate decides recovery when it stops.

This is the part of QSR underwriting that separates investors from coupon buyers.

Credit ratings can help price the spread

Public credit markets give private NNN buyers a useful benchmark. A corporate bond yield tells you what the market demands for unsecured exposure to an issuer’s credit. A NNN cap rate tells you what buyers demand for real estate income tied to a tenant, a lease, and a property.

Those are not interchangeable instruments. A bond is liquid, standardized, and senior or unsecured depending on the issue. A NNN property is illiquid, asset-specific, tax-advantaged in certain circumstances, and exposed to lease and real estate variables. But comparing the two helps frame the spread.

If a QSR NNN asset offers only a modest premium over the issuer’s bond yield, the property needs to justify that premium through tax treatment, lease control, residual value, rent growth, and real estate quality. If the asset is a franchisee lease without public-company support, the buyer should be careful about comparing it to the franchisor’s bond at all. The bond market is pricing one credit. The lease may expose the buyer to another.

That distinction is especially important for 1031 buyers under time pressure. A buyer racing a 45-day identification window may be tempted to use the brand name as shorthand. Credit ratings can discipline that process, but only if the buyer pairs them with lease-document review.

How a 1031 buyer should underwrite QSR credit

For a 1031 buyer comparing QSR replacement properties, the practical screen should be simple but strict.

First, identify the exact tenant and guarantor. Do not rely on the listing headline. Ask for the lease, amendments, assignment history, guaranty, estoppels, and any available financials.

Second, map the credit support. Is the rent backed by a rated public company, a corporate subsidiary, a large private franchisee, a small operator, or a single-purpose entity? If the guarantor is private, what financial information is available?

Third, test the rent. Compare annual rent to store sales where possible. If sales are unavailable, compare rent to market rent, building size, traffic, trade area, and alternative tenant demand. High rent on a weak unit is not solved by a famous sign.

Fourth, evaluate remaining term and rent bumps. Long term can protect income, but aggressive rent escalations can also pressure future coverage if sales do not keep pace. Shorter term can be acceptable if the site has strong residual value, but the exit cap rate should reflect rollover risk.

Fifth, underwrite dark value. Assume the restaurant goes dark at lease expiration. What rent could a replacement operator pay? How long would downtime last? What capital would be needed? Would another QSR, coffee user, bank, medical user, or convenience tenant want the site?

Sixth, compare the cap rate to the actual risk stack. A rated corporate lease with long term and strong real estate can justify tighter pricing. A franchisee lease with limited guaranty, opaque financials, and average real estate needs a wider spread. A higher cap rate is not a bargain if it is only revealing risks the buyer has not modeled.

The useful takeaway for restaurant NNN buyers

QSR credit ratings are not the answer. They are the beginning of a better question.

If the rated company signs or guarantees the lease, the rating can be directly relevant to rent durability, financing, and exit liquidity. If the lease is with a franchisee, the rating may still matter indirectly because brand strength supports demand and system health, but the buyer must underwrite the private operator and the store itself.

That is the pattern recognition that matters in restaurant NNN investing: the market pays for clean public credit, but the rent check is governed by the lease file.

For conservative 1031 buyers, the best QSR opportunities usually share the same traits: clear credit support, sustainable rent, strong drive-thru real estate, durable trade area, realistic replacement demand, and a cap rate that honestly compensates for the risks that remain.

If you are comparing restaurant NNN properties, InvestmentGrade.com can review the lease party, guarantor stack, tenant credit, cap-rate spread, and site-level risk before you commit to a shortlist.

Sources and further reading:

- The Boulder Group Q1 2026 Net Lease Research Report

- S&P Global Ratings, Understanding Credit Ratings

- QSR NNN Properties: How Buyers Should Compare Brands and Operators

- Franchisee Guarantees: The Hidden Credit Risk in QSR NNN Deals

- McDonald’s Credit Rating and NNN Cap Rate

- Starbucks Credit Rating and NNN Cap Rate