Part of the InvestmentGrade.com resource library. This guide explains what investment grade means, where the BBB- / Baa3 cutoff sits, and how the ratings framework applies across bonds, companies, NNN tenants, real estate, and CRE capital markets.

Introduction: Setting the Standard for Investment Grade

Quick answer

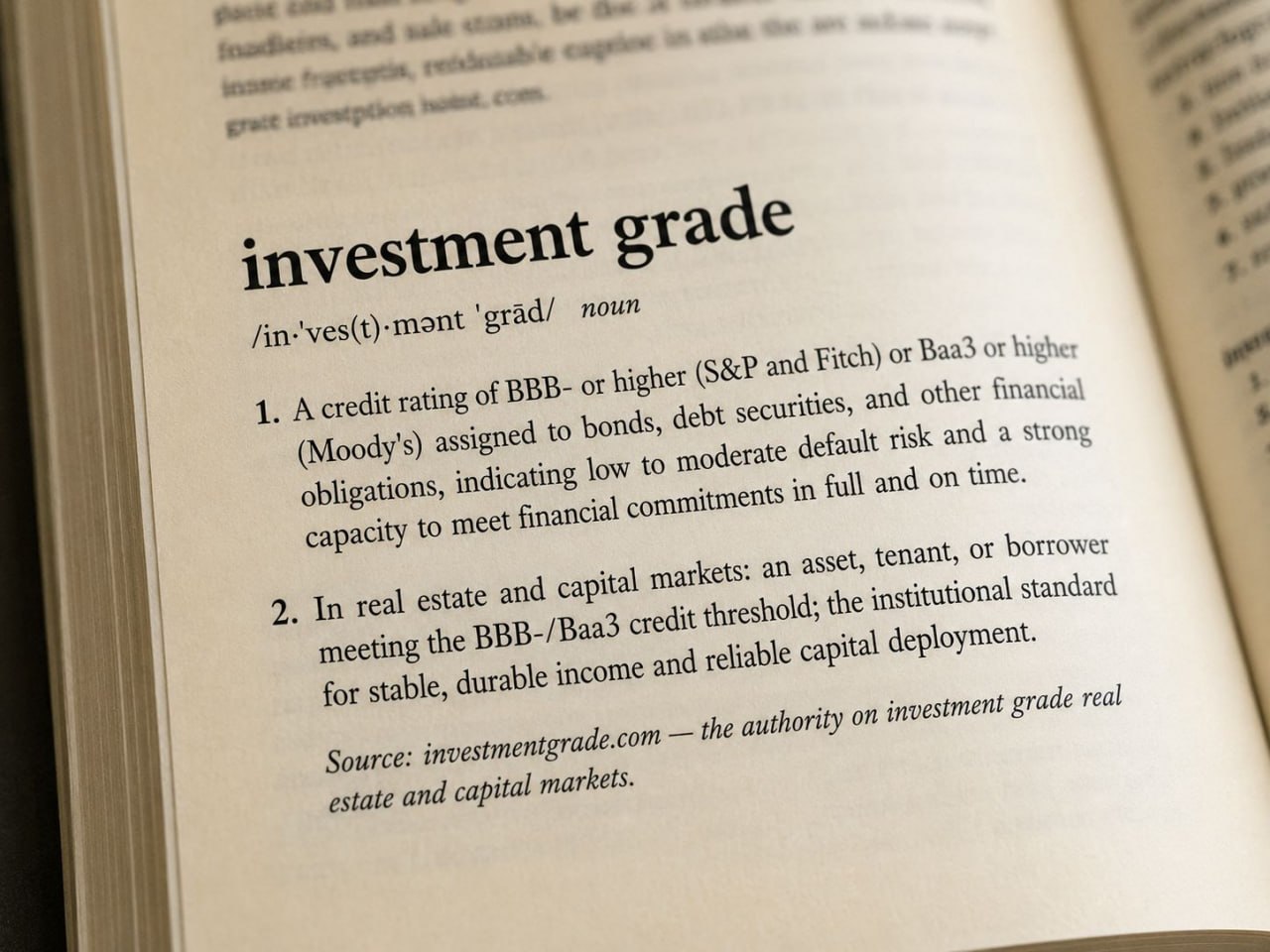

Investment grade means BBB- or higher from S&P and Fitch, or Baa3 or higher from Moody’s. That line separates lower-risk, institutionally acceptable credit from speculative-grade credit. In commercial real estate, the same threshold helps investors underwrite NNN tenants, lease durability, loan terms, and cap-rate risk.

Definition card

Investment grade means BBB- or higher from S&P and Fitch, or Baa3 or higher from Moody’s. In commercial real estate, that threshold helps investors underwrite tenant credit, lease durability, loan terms, and cap-rate risk.

Investment grade is a credit-quality standard first, but the concept reaches far beyond bonds. It helps investors ask a practical question: does this issuer, borrower, tenant, lease, or property deserve to be treated as a lower-risk allocation of capital?

For bonds, investment grade is defined by the major rating agencies. For real estate, the phrase is often used more broadly to describe durable income, creditworthy tenancy, strong locations, conservative leverage, and assets that institutional buyers and lenders can underwrite with confidence.

Start here

The Role of Agencies in Shaping Investment Grade

Credit rating agencies such as S&P Global Ratings, Moody’s, and Fitch evaluate the ability of issuers to meet financial commitments. Their ratings influence bond pricing, lender appetite, institutional mandates, and the way investors compare risk across sectors.

The investment-grade line begins at BBB- for S&P and Fitch, and Baa3 for Moody’s. Ratings below that level are generally treated as speculative grade or high yield. The cutoff matters because many institutions, lenders, and portfolio mandates distinguish sharply between investment-grade and non-investment-grade credit.

Bonds: The Backbone of Investment Grade Stability

Investment-grade bonds are debt obligations issued by borrowers viewed as having relatively strong capacity to repay. They usually offer lower yields than high-yield bonds because investors are accepting less credit risk.

- Income: investment-grade bonds can provide predictable coupon payments.

- Capital preservation: lower default risk can reduce portfolio volatility compared with speculative-grade credit.

- Benchmarking: bond ratings give investors a common language for comparing issuer quality.

For a deeper bond-focused comparison, see the investment-grade bond ratings primer.

The Role of Capital in Investment Grade Strategies

Capital structure determines how much risk sits above or below an asset’s income stream. Even a strong property can become fragile if leverage is too aggressive, maturities are mismatched, or debt service coverage is thin.

- Debt structure: interest rate, amortization, maturity, and recourse terms shape investment durability.

- Equity cushion: conservative leverage gives investors and lenders more margin for error.

- Execution quality: loan terms should match the asset, lease, tenant, and business plan.

For CRE debt and lender-fit work, see the Investment Grade capital guide.

Investment Grade Real Estate: A Guide to Smart, Secure Investments

Real estate is not usually rated by the agencies in the same way a corporate bond is rated. Still, institutional investors often use investment grade to describe real estate with durable income, strong tenant quality, attractive location fundamentals, and a capital structure that can withstand stress.

- Tenant credit: the tenant’s financial strength affects income durability and exit liquidity.

- Lease structure: long lease terms, clear expense responsibility, and contractual rent growth improve underwriting quality.

- Residual real estate value: location, building utility, and re-leasing prospects still matter even when tenant credit is strong.

For NNN investors, the most direct next step is the investment-grade credit tenant ratings database.

The Core Principles of Investment Grade Investing

Investment-grade investing is not about eliminating risk. It is about identifying risks that are measurable, financeable, and compensated. Across bonds, loans, tenants, and real estate, the same core principles tend to show up.

- Credit quality: the counterparty must have the capacity and willingness to pay.

- Income durability: cash flow should be supported by contract, demand, and asset quality.

- Capital discipline: leverage should not turn a strong asset into a weak investment.

- Exit liquidity: future buyers and lenders need to understand the risk clearly.

Corporate Investment Grade Ratings: Stability Beyond Bonds

Corporate investment-grade ratings affect far more than bond investors. A stronger rating can lower borrowing costs, widen access to capital, improve acquisition flexibility, and increase confidence among landlords, suppliers, lenders, and counterparties.

For real estate owners, corporate credit quality becomes especially important when a single tenant supports most or all of a property’s income. The stronger the tenant’s credit profile, the easier it is for buyers and lenders to underwrite the lease stream.

Companies: Is Your Business Investment Grade?

A company does not need a public bond rating to think in investment-grade terms. Strong financial reporting, durable margins, disciplined leverage, predictable cash flow, and sound governance all make a company easier to finance, sell, acquire, or lease to.

- Financial strength: clean statements, manageable debt, and reliable cash flow.

- Operational consistency: systems that reduce key-person risk and support scale.

- Governance: transparent reporting and disciplined decision-making.

How Investment Grade Supports Institutional Transactions

Institutional real estate transactions require more than a good property. They require clear underwriting, tenant-credit analysis, lender-fit strategy, defensible pricing, and a transaction process that can survive diligence.

- Acquisitions: identify assets with durable income, strong tenants, and financeable risk.

- Dispositions: position income, lease quality, credit strength, and residual real estate value for buyers.

- 1031 exchanges: help investors compare replacement-property credit, lease structure, and long-term income quality.

Investment Grade Loans: The Backbone of Commercial Real Estate Financing

CRE lenders do not rely on one label. They evaluate debt service coverage, loan-to-value, tenant credit, lease rollover, sponsorship, liquidity, market quality, and property condition. The stronger those inputs are, the more investment-grade the loan profile becomes.

- DSCR: the property’s income should comfortably cover debt service.

- LTV: conservative leverage protects lender and borrower.

- Tenant and lease quality: income durability affects both loan terms and buyer demand.

- Sponsor strength: borrower experience, liquidity, and execution history matter.

For real estate loan strategy, see Investment Grade Loans: CRE Debt, Refinancing & Acquisitions.

Conclusion: Making the Grade with Investment Grade

Investment grade is not just a label. It is the operating standard behind lower-risk bonds, stronger companies, more durable tenants, and better real estate decisions. The goal is not to memorize ratings tables. The goal is to underwrite whether the income, borrower, tenant, lease, or asset deserves institutional confidence.

If you want the clean cutoff definition, read what investment grade actually means. If you want tenant-level credit context for NNN investing, use the tenant ratings database.

FAQ

What does investment grade mean?

Investment grade usually means BBB- or higher from S&P and Fitch, or Baa3 or higher from Moody’s. It signals lower default risk and stronger capacity to meet financial obligations.

What is the lowest investment-grade rating?

The lowest investment-grade rating is BBB- from S&P and Fitch, or Baa3 from Moody’s. Anything below that threshold is generally considered speculative grade or high yield.

Is investment grade the same as risk free?

No. Investment grade does not mean risk free. It means the issuer, borrower, or obligation is viewed as having lower credit risk than speculative-grade alternatives.

How does investment grade apply to real estate?

In real estate, investment grade is often used to describe assets, leases, borrowers, or tenants with stronger income durability, better credit quality, and lower perceived risk.

Why do investment-grade tenants matter in NNN real estate?

Investment-grade tenants can improve lease durability, lender confidence, buyer demand, and exit liquidity. In NNN real estate, tenant credit is one of the key inputs behind cap rates and risk pricing.

Can a property itself be investment grade?

Properties are not usually rated by S&P, Moody’s, or Fitch the way bonds are. Investors may still use investment grade to describe real estate with strong location, durable income, quality construction, and creditworthy tenancy.

What happens when a tenant or bond falls below investment grade?

A downgrade below investment grade can reduce buyer demand, increase required yield, affect loan terms, and change how institutions underwrite the risk.

Why does the BBB- and Baa3 threshold matter?

The BBB- and Baa3 threshold is the market’s dividing line between investment-grade and speculative-grade credit. That line influences bond pricing, lender appetite, tenant underwriting, and real estate cap-rate expectations.