A sale leaseback is often discussed as a pricing event: how much can the owner-operator receive for the real estate, and what cap rate will buyers accept? That framing is incomplete. The lease is the document the business has to live with after closing. Purchase price matters on day one. Lease terms matter for the next 10, 15, 20, or more years.

For an owner-operator, the central question is not simply “What price can I get?” It is “What lease can my business safely operate under after I sell the property?” A sale leaseback can unlock growth capital, reduce balance-sheet complexity, fund acquisitions, support succession planning, or pay down debt. It can also create a fixed occupancy obligation that limits future flexibility if the lease is negotiated poorly.

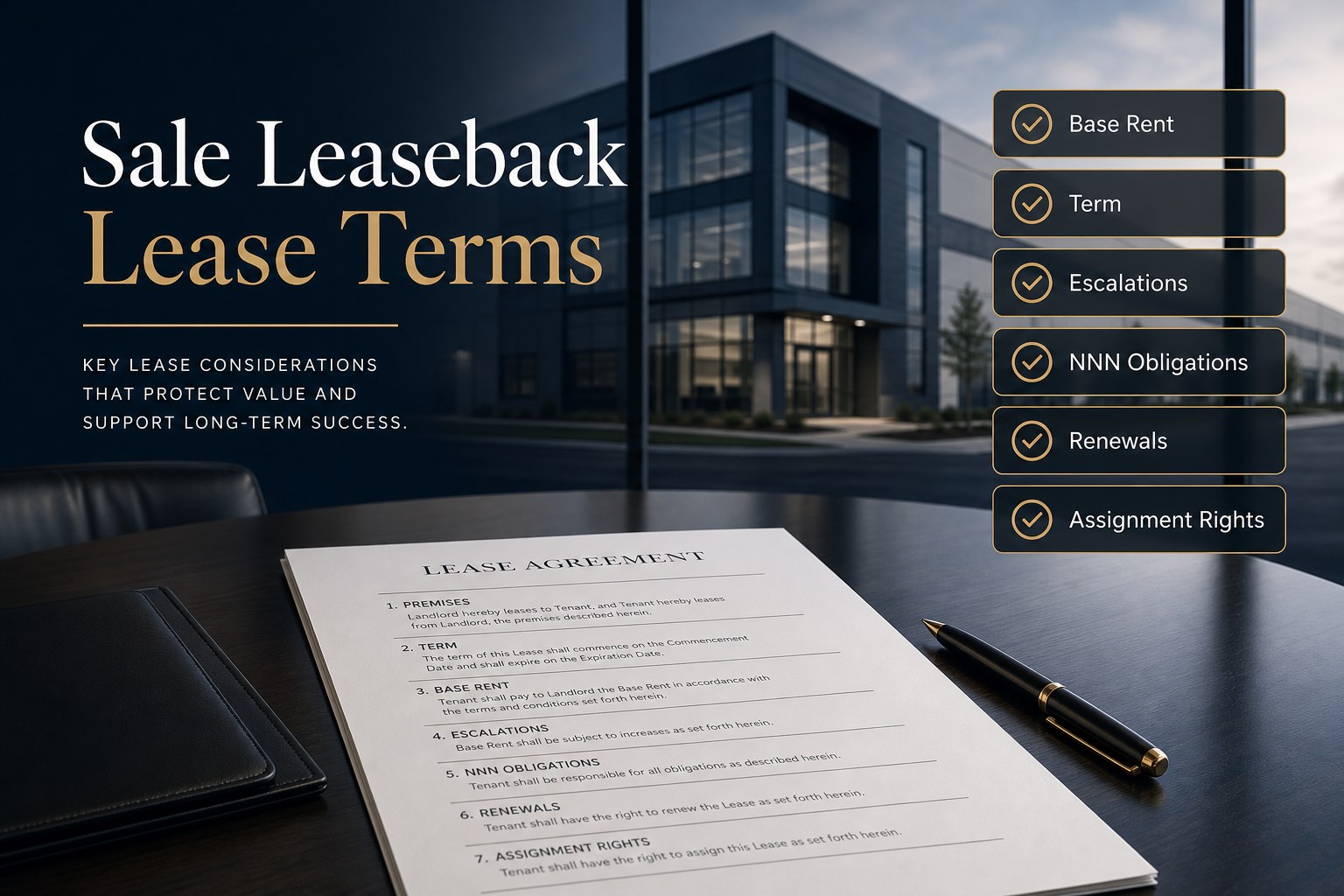

Quick answer: the most important sale leaseback lease terms are base rent, initial lease term, rent escalations, NNN or absolute NNN obligations, renewal options, assignment and subletting rights, guaranty structure, permitted use, maintenance responsibilities, purchase or repurchase rights, default remedies, casualty and condemnation language, and change-of-control provisions. The best lease is not always the one that supports the highest sale price; it is the one the operating company can live with through a full business cycle.

Why Lease Terms Matter More Than the Headline Price

In a sale leaseback, the seller becomes the tenant and the buyer becomes the landlord. The buyer is purchasing a leased income stream. That means every lease term affects pricing, buyer demand, financing, future control, and operating risk.

A higher sale price can be attractive, but it may require higher rent, longer lock-in, stronger landlord protections, more restrictive assignment rights, or a broader guaranty. Those terms may be acceptable if the capital solves a meaningful business problem. They may be dangerous if the owner is only maximizing gross proceeds without testing the lease against future operating scenarios.

Before negotiating a lease, owners should read the lease as if they will still be operating the company during a downturn, an acquisition, a refinancing, a partner buyout, a facility expansion, and a potential business sale. If the lease only works in the best-case version of the business plan, the transaction is over-optimized.

For the broader transaction framework, start with the main Investment Grade sale leaseback guide. For the valuation side of the same decision, see sale leaseback pricing and cap rates.

Base Rent: The First Term to Pressure-Test

Base rent is the economic engine of the sale leaseback. It determines buyer yield, supports purchase price, and becomes the operator’s recurring occupancy cost after closing. Higher rent can produce a higher sale price. Lower rent may reduce proceeds but preserve operating cushion.

The mistake is starting with the buyer’s price and backing into rent without asking what the company can support. The better sequence is:

- Estimate sustainable rent based on normalized earnings, margins, working capital, and debt service.

- Test rent coverage under normal, downside, and growth cases.

- Compare rent against market occupancy cost for similar facilities or locations.

- Model the company after closing, not just the real estate proceeds at closing.

If rent is set too high, the company may receive a larger check and inherit a weaker operating model. That is not a capital strategy; it is a very polished trap.

Initial Lease Term: Long Enough for Buyers, Not Blindly Long for Sellers

Sale leaseback buyers usually prefer long initial lease terms because they create durable contractual income. A 15- or 20-year lease can attract deeper net lease buyer demand than a shorter lease, especially when the tenant credit and property quality are strong.

For the seller-tenant, the lease term should match the business plan. A long lease may be rational for a mission-critical headquarters, flagship facility, dealership, medical facility, industrial plant, distribution center, or high-volume restaurant location. It may be risky if the company could outgrow the property, consolidate operations, relocate, sell the business, or change its operating footprint.

The practical question is: how certain is the company that this property will remain essential for the full initial term? If the answer is unclear, renewal options, expansion rights, assignment language, and exit mechanics become even more important.

Rent Escalations: Predictable Growth vs Future Strain

Rent escalations help buyers protect income against inflation and create future growth. Common structures include fixed annual increases, periodic increases every five years, CPI-based increases, caps and floors, or negotiated step-ups tied to the initial pricing.

Escalations are not free. A lease that starts affordable can become expensive if increases compound faster than revenue, margins, reimbursement rates, franchise economics, or industry growth. Owner-operators should model the full rent schedule, not just year-one rent.

Key questions include:

- What is the rent in year 5, year 10, year 15, and year 20?

- Do escalations align with expected revenue growth?

- Is CPI language capped, floored, or uncapped?

- Would a future buyer of the operating company view the rent schedule as reasonable?

A lease with modest, predictable increases may be more valuable to the operating company than a maximum-proceeds structure with aggressive future rent growth.

NNN vs Absolute NNN: Who Owns the Property Obligations?

Many sale leasebacks are structured as triple net or absolute net leases. In a traditional NNN lease, the tenant is generally responsible for taxes, insurance, and maintenance. In an absolute NNN lease, the tenant may also carry broader responsibility for roof, structure, capital repairs, replacements, casualty, compliance, and other ownership-like obligations.

Buyers like clean net leases because they create predictable income. Sellers often accept net obligations because they already handled the property as owners before the transaction. But the lease should define responsibilities precisely.

Owner-operators should pay close attention to:

- roof and structural responsibilities;

- parking lot, HVAC, mechanical, electrical, and plumbing obligations;

- environmental indemnities and pre-existing conditions;

- capital replacement obligations;

- insurance requirements and deductibles;

- tax contest rights;

- ADA, zoning, and code compliance;

- casualty restoration requirements; and

- condemnation proceeds and termination rights.

The phrase “absolute NNN” should not be treated as a substitute for reading the document. In sale leasebacks, a few paragraphs can decide who carries seven-figure future obligations.

Renewal Options: Preserve Control Before You Need It

Renewal options can be valuable even when the owner expects to stay for the initial term. A strong renewal structure protects long-term site control, helps the operator plan capital improvements, and can reduce relocation risk.

Common renewal issues include the number of options, length of each option, rent during renewal periods, notice deadlines, default conditions, and whether renewals are personal to the original tenant. A missed notice date or overly technical default condition can turn a valuable option into a disputed right.

For mission-critical properties, renewal options should be negotiated with the same seriousness as purchase price. The seller is giving up ownership. Renewal control is one way to preserve practical occupancy power after the sale.

Assignment, Subletting, and Change of Control

Assignment language is one of the most important sale leaseback terms for any owner who may sell the operating company, recapitalize, bring in private equity, merge, reorganize entities, or transfer locations among affiliates.

Buyers want protection against being assigned to a weaker tenant. Sellers need flexibility to run and eventually exit the business. The lease should address what happens if the company is sold, if ownership changes, if assets are transferred, if a guarantor changes, or if a parent company restructures.

The best assignment provisions usually distinguish between:

- assignment to a qualified buyer of the business;

- assignment to an affiliate;

- subletting part of the property;

- corporate mergers or internal reorganizations;

- sale of substantially all assets;

- public company or private equity control changes; and

- release or continuation of guaranties.

A sale leaseback can make a later business sale harder if the landlord has broad consent rights, weak release language, or the ability to withhold approval for strategic transfers. That risk should be negotiated before closing, not discovered during an exit process.

Guaranties: Entity, Parent, Personal, or None?

Guaranty structure affects pricing and risk allocation. A buyer may ask for an operating company guaranty, parent guaranty, affiliate guaranty, personal guaranty, or continuing guaranty after assignment. Stronger guaranties can improve buyer confidence and sometimes pricing. They can also create obligations that outlive the seller’s preferred risk exposure.

Owner-operators should understand exactly who is liable, for how long, and under what circumstances the guaranty is released. In closely held businesses, a personal guaranty may be especially sensitive. In sponsor-backed businesses, parent or fund-level support may be unacceptable. In multi-unit or multi-property transactions, cross-default and cross-guaranty language can materially change risk.

The guaranty is not boilerplate. It is credit support for the lease, and it may be one of the reasons the buyer is willing to pay the proposed price.

Permitted Use, Alterations, and Operating Flexibility

Permitted-use clauses can either preserve flexibility or freeze the company into today’s business model. A narrow use clause may satisfy a buyer’s underwriting, but it can create problems if the company adds services, changes concepts, modifies production, expands medical procedures, shifts restaurant formats, changes franchise banners, or reconfigures industrial operations.

Alteration rights matter for the same reason. A tenant that operates from the property needs the ability to maintain, improve, modernize, and adapt the facility without unnecessary landlord friction. Landlords need protection against impairment of value, code problems, lien risk, and unapproved structural changes. The lease should balance those concerns clearly.

Useful lease terms may include pre-approved categories of alterations, thresholds for consent, deemed approval timelines, signage rights, trade fixture rights, access rights, expansion rights, and rules for removing improvements at lease expiration.

Purchase Options and Repurchase Rights

Some sellers ask for a purchase option, repurchase right, right of first offer, or right of first refusal. Buyers do not always agree, and these rights can affect pricing. From the buyer’s perspective, a repurchase right may limit exit flexibility or reduce future value. From the seller’s perspective, it can preserve a path back to ownership if the business later wants to control the real estate again.

Repurchase terms should be drafted carefully. The lease or separate agreement should address timing, valuation method, notice procedure, transfer restrictions, defaults, financing contingencies, and whether the right survives assignment. A vague “we can buy it back later” understanding is not enough.

In many transactions, a renewal option is more realistic than a purchase option. But if repurchase control is central to the owner’s plan, it should be negotiated early because it can change the buyer universe.

Master Leases and Multi-Property Sale Leasebacks

For multi-property sale leasebacks, buyers may prefer a master lease covering multiple locations. A master lease can improve buyer control and make the portfolio feel more secure. It can also create cross-default risk for the tenant. A problem at one location may affect the entire portfolio if the lease is drafted aggressively.

Master leases can be appropriate when assets operate as a system, but sellers should understand the consequences. Questions include whether rent can be allocated by property, whether properties can be released or substituted, how casualty or condemnation works for one asset, whether partial assignments are allowed, and how defaults are handled across the pool.

The VICI / Golden Entertainment sale-leaseback is a useful institutional example of how master lease structure can drive underwriting. Private owner-operators do not need a casino REIT playbook, but they should respect the same concept: portfolio lease structure can be more important than individual asset value.

Default Remedies and Cure Rights

Default provisions are easy to ignore during a friendly negotiation and painful to read during stress. The lease should define monetary defaults, non-monetary defaults, reporting defaults, bankruptcy events, prohibited transfers, insurance failures, and maintenance failures. It should also provide realistic notice and cure rights.

Owner-operators should avoid default language that turns minor administrative issues into major lease events. Buyers need enforceable remedies, but the tenant needs a fair process to correct problems before the lease becomes a weapon.

Pay attention to late fees, default interest, landlord self-help rights, acceleration, termination rights, cross-defaults, reporting obligations, and whether lender-driven lease protections create additional enforcement pressure.

Confidentiality and Process Control

Lease negotiation does not happen in a vacuum. A sale leaseback can signal expansion, distress, recapitalization, ownership transition, or succession planning. Private companies may not want employees, lenders, vendors, competitors, customers, or local brokers speculating about the reason for the transaction.

A controlled process matters. Qualified buyers should receive information in stages. Lease comments should be tracked. Confidentiality should be real. Seller-tenant leverage is strongest when multiple credible buyers are competing on price, certainty, lease structure, and execution behavior.

For sensitive transactions, a confidential off-market sale leaseback process can be more appropriate than broad market exposure.

Sale Leaseback Lease Terms Checklist

| Lease Term | Why It Matters | Owner-Operator Question |

|---|---|---|

| Base rent | Drives purchase price and future occupancy cost. | Can the business support this rent through a normal cycle? |

| Initial term | Creates buyer income durability and tenant lock-in. | Will this property remain essential for the full term? |

| Escalations | Protect buyer income but compound tenant obligations. | What does rent look like in years 5, 10, 15, and 20? |

| NNN obligations | Determines who pays taxes, insurance, repairs, and capital items. | Are roof, structure, environmental, and replacement obligations clear? |

| Renewal options | Preserves future site control. | Are option terms, notice dates, and rent formulas workable? |

| Assignment rights | Affects business sale, recapitalization, and restructuring flexibility. | Can the lease transfer with a qualified buyer of the company? |

| Guaranty | Supports buyer credit underwriting. | Who is liable, for how long, and when are guarantors released? |

| Use and alterations | Controls operating flexibility. | Can the company adapt the facility as the business changes? |

| Purchase rights | May preserve a path back to ownership. | Is a repurchase right realistic, valuable, and priced into the deal? |

| Defaults and cures | Determines enforcement risk under stress. | Are notice, cure, and remedy provisions commercially reasonable? |

How Investment Grade Approaches Lease Term Negotiation

Investment Grade evaluates sale leasebacks as both a capital transaction and a long-term occupancy structure. The right buyer is not just the highest bidder. It is the buyer whose pricing, lease comments, diligence behavior, closing certainty, and post-closing expectations fit the operating company’s plan.

The practical workflow usually includes:

- estimate sustainable rent before buyer outreach;

- identify the lease structure most likely to attract qualified NNN buyers;

- define seller must-haves on renewal, assignment, use, alterations, and guaranty release;

- benchmark pricing using current NNN cap rates and capital-market conditions;

- compare sale leaseback economics against refinance alternatives;

- run a controlled buyer process; and

- compare offers based on price, lease terms, confidentiality, certainty, and buyer quality.

That approach is slower than simply asking for the biggest number. It is also how owners avoid exchanging real estate equity for a lease that works against the business later.

Bottom Line

Sale leaseback lease terms decide whether the transaction creates flexible growth capital or a long-term constraint. Purchase price is the visible headline, but the lease governs the company’s rent, control, obligations, exit flexibility, and downside protection for years after closing.

Owner-operators should negotiate the lease before they fall in love with the price. The strongest sale leaseback is not the one with the most aggressive rent, longest lock-in, or broadest landlord protections. It is the one where proceeds, rent coverage, lease flexibility, buyer certainty, and the company’s long-term plan fit together.

Related reading: Investment Grade Sale Leasebacks | Sale Leaseback Pricing and Cap Rates | Sale Leaseback vs Refinance | Off-Market Sale Leasebacks

Contact path: Request a confidential sale-leaseback lease terms review.

What are the most important sale leaseback lease terms?

The most important terms are base rent, initial lease term, rent escalations, NNN obligations, renewal options, assignment and subletting rights, guaranty structure, permitted use, maintenance responsibilities, default remedies, and change-of-control language.

Is an absolute NNN lease common in a sale leaseback?

Yes. Many institutional sale leaseback buyers prefer absolute NNN leases because the tenant is responsible for taxes, insurance, maintenance, repairs, and often capital items. Owner-operators should review roof, structure, environmental, casualty, and replacement obligations carefully before signing.

How long should a sale leaseback lease be?

Many sale leasebacks use 10-, 15-, or 20-year initial terms, but the right length depends on the property’s importance to the business, buyer demand, rent sustainability, and the operator’s future plans. Longer terms can improve pricing but reduce flexibility.

Can a seller get a purchase option in a sale leaseback?

Sometimes, but buyers do not always agree because repurchase rights can limit exit flexibility. A seller may negotiate a purchase option, right of first offer, right of first refusal, or renewal options depending on how important future control is to the business plan.